The 50/30/20 budget rule has been around long enough to have its own fan club and its own support group. It promises simplicity — split your after-tax income into three buckets, call it a day, go live your life. And for a lot of people, that simplicity is exactly what made it click when nothing else had.

But rent is not what it was when this rule got popular. Groceries are not what they were two years ago. So the reasonable question is: does the 50/30/20 rule still work today, or has real life quietly outgrown it?

The honest answer is: it depends on what you need from a budgeting method. Let’s walk through how it actually works, where it holds up, where it struggles, and how to adapt it without throwing the whole framework out.

The 50/30/20 Budget Rule Explained (The Short Version)

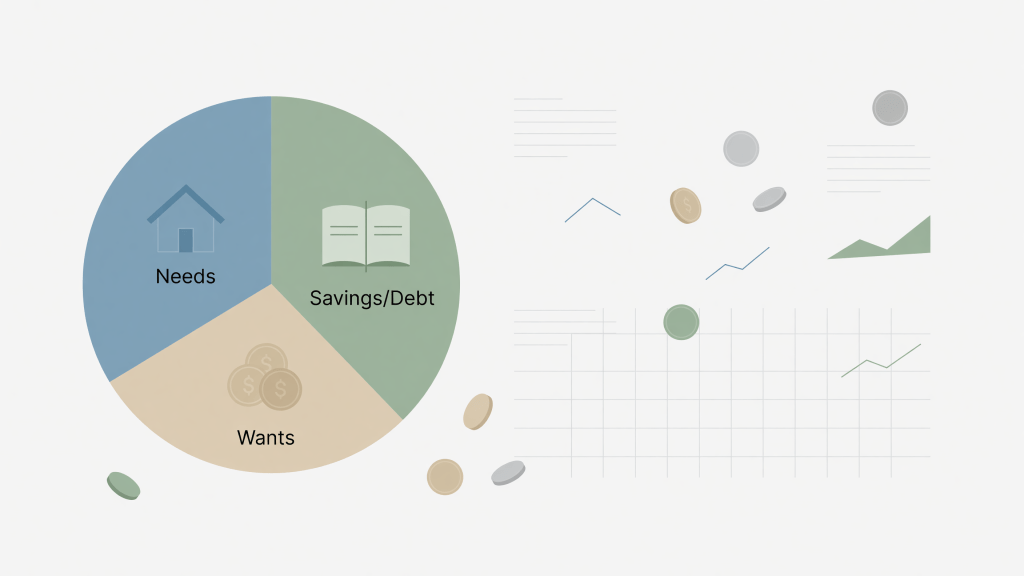

The idea is straightforward. Take your monthly after-tax income and divide it like this:

- 50% toward needs — rent or mortgage, utilities, groceries, transportation, minimum debt payments, insurance. The fixed expenses and near-fixed expenses that would cause real problems if you skipped them.

- 30% toward wants — dining out, streaming subscriptions, travel, hobbies, the things that make life feel like a life rather than a spreadsheet.

- 20% toward savings and debt repayment — your emergency fund, retirement contributions, extra debt payments, and anything you’re building toward.

That’s the whole rule. No envelope system, no daily tracking, no color-coded categories for every possible human purchase. For someone who has never budgeted before, or who has tried more complicated systems and quietly stopped using them by the ninth of the month, this framework lowers the activation energy considerably.

It’s also the closest thing budgeting has to a “good enough” starting point. And good enough that you actually use beats perfect that you abandon.

The 50/30/20 Rule With High Cost of Living: Where It Gets Complicated

Here is where the honest conversation starts. In many cities, housing alone will consume 40 to 50 percent of a moderate income before you’ve bought a single bag of groceries. When your fixed expenses are already at the ceiling of the “needs” bucket, the 30/20 split on the remaining half has nowhere to breathe.

This is not a personal failure. It is a math problem, and math problems have adjustments.

A few adaptations that keep the spirit of the method without pretending your rent is different than it is:

- Shift to a 60/20/20 split temporarily, treating the extra 10% taken from “wants” as a structural reality rather than overspending. Review it every few months as income grows or expenses shift.

- Use it as a direction, not a destination. If you’re at 62/28/10 right now, the goal is to gradually move toward 50/30/20 — not to feel disqualified from budgeting because you’re not there yet.

- Separate your savings rate from the percentages. Even a consistent 10% savings rate, maintained month after month, compounds meaningfully over time. The FIRE community tracks savings rate obsessively for exactly this reason — it’s the number that actually predicts long-term financial outcomes.

The 50/30/20 rule is a framework, not a law. Frameworks bend. Laws don’t. You want a framework.

50/30/20 Budgeting Method Pros and Cons (The Unvarnished List)

Where it works well:

- It’s fast to set up. You can do a first draft in under twenty minutes with a calculator and your last pay stub.

- It doesn’t require tracking every purchase in real time, which is the part that quietly kills most budgets.

- The 20% savings allocation is built into the structure from the start, which means saving isn’t treated as whatever’s left over at the end of the month (which, famously, is often zero).

- It’s flexible enough to accommodate irregular income if you base the percentages on a conservative baseline income figure and treat anything above that as a bonus round.

Where it runs into trouble:

- It doesn’t distinguish between an emergency fund and retirement savings, which are solving very different problems. An emergency fund is your cash cushion — the thing that keeps a broken transmission from becoming credit card debt. A sinking fund handles the annual expenses you can see coming. Retirement savings are a third category entirely. Lumping all three into “20%” without a plan often means one of them doesn’t get funded.

- The “wants” bucket is where subscription audits go to die. Streaming services, gym memberships, software trials from 2022 — the subscriptions are not hiding; they are just very committed to staying employed. The 30% wants category can silently absorb things you forgot you were paying for.

- It doesn’t connect directly to your net worth. You can follow the 50/30/20 rule faithfully and still have no clear picture of whether your total financial position is improving. Net worth — assets minus liabilities — is the number that actually tells you whether your budget is working over time, and the basic rule doesn’t surface that.

How to Use 50/30/20 Budgeting to Actually Build Net Worth

This is where personal finance budgeting techniques either connect to real outcomes or stay theoretical. The 50/30/20 rule gets you organized. Building net worth requires one additional habit: knowing where you actually stand.

Net worth is assets minus liabilities. Assets are what you own — checking and savings balances, retirement accounts, property, investment accounts. Liabilities are what you owe — mortgage balance, car loans, student loans, credit card balances. The difference is your net worth. It is not your income, not your salary, not your credit score. It’s the number that measures progress over time.

According to the Federal Reserve Survey of Consumer Finances, median household net worth in the US was approximately $192,000 as of their most recent data. But that number varies enormously by age, region, and family structure — so treat it as context, not a benchmark you need to hit by a certain birthday.

What matters more than the number itself is whether it’s moving in the right direction. And that’s where a weekly money check-in earns its keep.

Once a week — ten minutes, not a production — look at three things: your account balances, your spending against your budget categories, and your net worth figure. Weekly check-ins tend to stick better than daily tracking because they’re frequent enough to catch drift early but not so constant that the whole thing starts to feel like a second job. You’re not grading yourself. You’re just looking.

When you can see your savings rate climbing and your liabilities shrinking in the same view, the budget stops feeling like a restriction and starts feeling like a tool that’s working. That’s the shift from budgeting as performance to budgeting as strategy — which is also, not coincidentally, how budgeting strategies for building net worth actually function in practice.

If you want a single place to run that weekly check-in without connecting every bank account to a third-party app, the Vault & Press Net Worth Tracker handles both the budget view and the net worth calculation in one spreadsheet. It’s the kind of tool that earns its keep by being genuinely fast to update — because if it takes more than ten minutes, most people stop doing it, and then the whole thing was theoretical anyway.

For more on the mechanics of building your number from scratch, this post on calculating net worth covers the liabilities side in particular, which is where most people accidentally undercount. And if you’re looking at your budget and realizing the 50/30/20 split might work better with a zero-based layer underneath it, the zero-based budgeting guide walks through how to give every dollar a job before the month begins — which pairs naturally with any percentage-based framework.

For further reading on budgeting frameworks and how they interact with savings behavior, the Consumer Financial Protection Bureau’s budgeting tools and the Federal Reserve Survey of Consumer Finances are both worth bookmarking — dry in places, genuinely useful in others.

Frequently Asked Questions

Is the 50/30/20 budget rule a good budgeting method for beginners?

Yes, for most people starting out. It gives you a structure without requiring granular tracking of every purchase. The main thing to add early is clarity about what sits inside your 20% — emergency fund, sinking funds, and retirement contributions are different tools, and the rule doesn’t sort that out for you.

What counts as a “need” versus a “want” in the 50/30/20 budget rule?

Needs are expenses where skipping them causes a real problem: housing, utilities, groceries, transportation to work, minimum debt payments, insurance. Wants are things that improve your quality of life but are genuinely optional: restaurants, subscriptions, travel, entertainment. The line can be blurry — a gym membership might be a need for some people’s mental health and a want for others. You get to make that call for your own budget.

What if my needs are already over 50% of my income?

Adjust the percentages to reflect your actual situation and use the 50/30/20 target as a direction rather than a requirement. Many people in high cost-of-living areas work with a 60/20/20 or even 65/15/20 split while actively working to shift the ratios over time. The goal is steady improvement, not immediate perfection.

How does the 50/30/20 budget rule connect to net worth?

The 20% savings piece is where the connection lives. The more consistently you fund savings and pay down liabilities, the more your net worth — assets minus liabilities — moves in the right direction. The budget creates the cash flow; net worth tracking shows you the cumulative result. Running both in a single spreadsheet makes it easier to see how monthly habits add up over time.

The 50/30/20 budget rule doesn’t need to be perfect to be useful. It needs to be simple enough that you actually run it, flexible enough to fit your real numbers, and connected to a net worth view so you can see whether the whole thing is moving in the right direction. That’s a pretty reasonable ask from a three-number framework.

Are you currently using the 50/30/20 rule, or have you adapted it into something that fits your situation better? Drop your version in the comments — there’s no wrong answer here, and someone else’s workaround might be exactly what another reader needs to hear.

{“@context”:”https://schema.org”,”@type”:”BlogPosting”,”headline”:”The 50/30/20 Budget Rule: Does It Still Work This Year?”,”description”:”The 50/30/20 budget rule explained for today’s cost of living. Learn how to adapt it, its pros and cons, and whether it can actually build your net worth.”,”keywords”:[“50/30/20 budget rule explained”,”does the 50/30/20 rule still work today”,”50/30/20 budgeting method pros and cons”,”how to budget with 50/30/20 rule”,”50/30/20 rule for saving money”,”budgeting strategies for building net worth”,”best budgeting methods for financial freedom”,”50/30/20 rule with high cost of living”,”personal finance budgeting techniques”,”how to increase net worth with a budget”],”datePublished”:”2026-07-03T21:20:05.263Z”,”dateModified”:”2026-07-03T21:20:05.263Z”,”author”:{“@type”:”Organization”,”name”:”The Skill Mill”},”mainEntityOfPage”:”https://blog.theskillmillbooks.com/the-50-30-20-budget-does-it-still-work-this-year-/?utm_source=skillmillblog&utm_medium=blog&utm_campaign=net-worth-and-budgeting&utm_content=the-50-30-20-budget-does-it-still-work-this-year-“}

Related Skill Mill reading

Tools that help: MineStock Pro.

Leave a comment